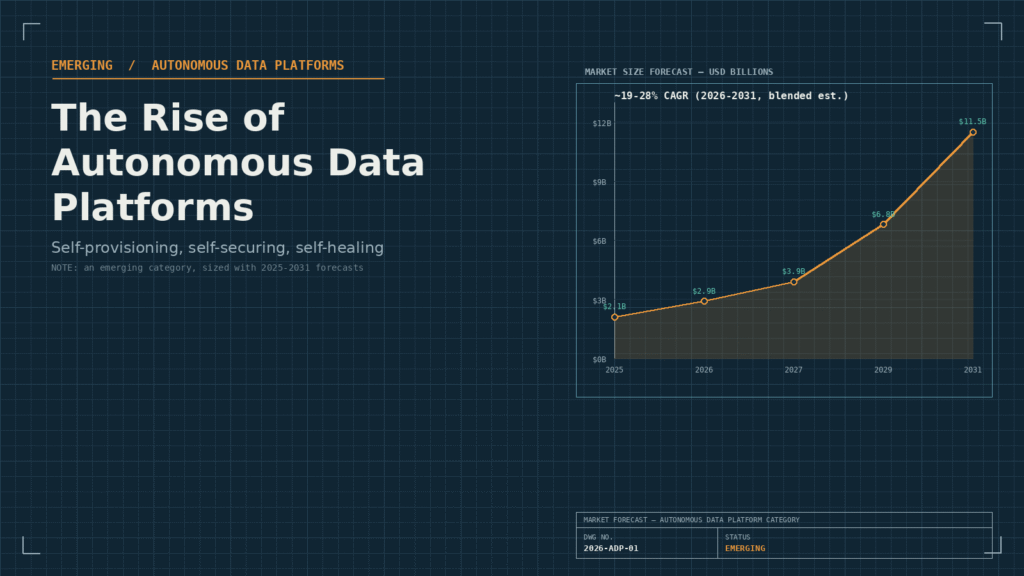

Every enterprise data stack eventually hits the same wall: more data sources, more pipelines, more compliance obligations, and not enough people to tune, patch, secure, and babysit all of it manually. Autonomous data platforms are the industry’s answer to that wall, and in 2026 they’ve moved from an emerging category to one of the fastest-growing segments in enterprise infrastructure. Market estimates vary by methodology, but they all point the same direction: figures for 2026 alone range from roughly $2.55 billion to $3.6 billion depending on the analyst, with forecasts converging on somewhere between $6 billion and $16 billion by the early 2030s, at compound annual growth rates commonly cited between 19% and 28%. That’s not incremental growth. That’s a category being built in real time.

What an Autonomous Data Platform Actually Is

An autonomous data platform (ADP) is an AI-powered database and data-management system built to automate the tasks that used to require a dedicated operations team: provisioning, tuning, patching, indexing, security enforcement, and lifecycle management. The goal isn’t just automation for its own sake — it’s minimal human involvement while maintaining, or improving, performance, reliability, and scalability. Where a traditional data platform waits for a database administrator to notice a slow query or a misconfigured access policy, an autonomous platform is designed to detect and correct those conditions itself, in real time, without a ticket ever being filed.

That distinction matters more than it sounds. Self-optimizing and self-securing behavior is what lets these platforms support faster decision-making at the business layer — not because the underlying data got faster to query, but because the friction of keeping the system healthy stopped consuming engineering time.

The Numbers Behind the Emerging Category

A few data points explain why this category is attracting so much investment right now.

Unstructured data is the dominant workload. Unstructured data processing commanded roughly 56% of the autonomous data platform market in 2025, with semi-structured workloads growing even faster — near a 30% compound annual growth rate through 2031. That’s a direct reflection of what modern enterprises actually generate: logs, documents, sensor streams, and multimedia, not the tidy relational tables these systems were originally designed around.

Large enterprises lead, but SMEs are catching up fast. Large enterprises account for more than 60–65% of current adoption, driven by data complexity and governance mandates that manual teams can no longer keep pace with. But the SME segment is the fastest-growing cohort, expanding at roughly 25% CAGR as pricing and onboarding simplify — cumulative SME contract value in this category is projected to reach around $9 billion in 2026 alone, driven heavily by embedded-finance software vendors, prop-tech firms, and telehealth startups.

Regional adoption is uneven but accelerating everywhere. North America holds the largest revenue share, generally cited around 40%, while Asia-Pacific is the fastest-growing region at roughly 22–28% CAGR depending on the source, fueled by rapid enterprise digitization in China, India, and Southeast Asia.

Specific verticals are moving first. Banking and financial services lead adoption at close to 22% market share, driven by real-time fraud detection needs. Healthcare and life sciences are close behind, expanding at roughly 25% CAGR as organizations process clinical and genomic datasets that are both massive and sensitive. Retail is the fastest-growing vertical overall, north of 26% CAGR, pushed by demand for personalized analytics and AI-driven inventory forecasting.

Real Numbers From Real Deployments

Market forecasts are useful, but the deployment-level data is where the case for autonomous platforms gets concrete.

A UK fintech processing roughly eight billion monthly payment events reported flagging fraudulent transactions within four seconds using built-in anomaly detection, and estimated the equivalent of three dozen engineer-months in annual manpower savings from not needing dedicated site-reliability staff for that workload. A global media company used dynamic warehouse auto-sizing to cut a 40-terabyte overnight processing window roughly in half. An e-commerce operation using automatic materialized-view refresh saved close to 10,000 compute hours annually. A consumer-goods company’s analytics workload hit a 90% cache-hit rate using automated query caching, without a database team manually tuning it.

None of these are hypothetical efficiency gains from a vendor’s slide deck — they’re the kind of operational math that shows up in a CFO’s infrastructure line item, which is exactly why adoption is accelerating past the early-adopter phase.

Why This Is Happening Now

Three forces are converging to push autonomous data platforms from “emerging” to “expected”:

Cloud maturity removed the infrastructure excuse. Hyperscalers have built autonomy directly into baseline cloud services — provisioning, governing, and scaling databases without specialized in-house skills is now closer to a default feature than a premium add-on. That shift alone accounts for a meaningful share of the category’s growth, since it lowers the bar to adoption for organizations without dedicated database teams.

Regulatory pressure is forcing governance to be automatic, not aspirational. The EU Data Act’s portability and residency mandates, alongside GDPR’s field-level lineage requirements, are pushing enterprises toward platforms that deliver automated compliance rather than manual catalog updates. Autonomous platforms that generate audit trails and lineage as a structural byproduct — not a separate project — are winning procurement decisions specifically because the compliance burden has gotten too large to handle manually. The consequences of getting this wrong are not abstract either: regulators have already issued significant fines tied to overlooked defaults in self-optimizing systems, which has sharpened enterprise attention on governance-by-design rather than governance-as-afterthought.

Agentic AI is reshaping what “autonomous” even means. Vendors across the market are actively building agentic data-management systems on top of their platforms — not just automating fixed rules, but layering AI agents that reason about workload placement, query optimization, and anomaly response dynamically. This is the leading edge of the category right now: the difference between a system that follows pre-set automation rules and one that adapts its own management strategy as conditions change.

What’s Still Holding Adoption Back

The growth numbers shouldn’t obscure the real friction points. Data privacy and regulatory compliance remain the most cited bottleneck slowing broader rollout — not because autonomous platforms are inherently less secure, but because handing more operational control to an automated system raises the stakes when something is misconfigured. Multiregional data-sovereignty requirements are forcing vendors to build increasingly complex replication and residency architectures just to stay compliant across jurisdictions, which adds cost and complexity even as it’s marketed as automation.

There’s also a skills gap on the buyer side. Managed-service offerings for these platforms are growing faster than self-managed deployments specifically because most organizations don’t yet have the in-house MLOps and governance expertise to run an autonomous platform confidently without vendor support — which somewhat undercuts the “minimal human involvement” pitch, at least for now.

Where This Goes From Here

The trajectory is fairly unambiguous even accounting for the spread between different market forecasts: autonomous data platforms are moving from a differentiator that early adopters used to win a competitive edge, toward baseline infrastructure that most mid-size and large enterprises will be expected to run. The vendors leading this shift — Oracle, Snowflake, Databricks, AWS, Microsoft, IBM, and a growing list of specialized challengers — are converging on the same feature set: self-provisioning, self-securing, self-healing, with agentic reasoning increasingly layered on top of static automation rules.

What makes this an emerging category worth watching closely, rather than just another infrastructure upgrade cycle, is the compounding effect. Every enterprise that adopts an autonomous platform reduces its own manual operational overhead, which frees engineering time for the next layer of automation, which in turn accelerates the case for the vendor’s next feature release. That feedback loop — not any single product launch — is what’s actually driving the growth curve underneath all these market forecasts.

For data teams evaluating whether to move now or wait, the honest answer from the 2026 data is: the platforms are mature enough to deliver measurable savings today, but governance and skills readiness, not the technology itself, are what will determine whether a given rollout succeeds.