Four of the “Magnificent Seven” companies alone are on track to spend roughly $650 billion on AI infrastructure capital expenditure in 2026 — a 71.1% jump year-over-year. That single figure captures how much of the US economy is now running through a fairly small set of companies building the chips, data centers, and cloud platforms underneath every American AI product. Nvidia projects industry-wide AI data center capex could reach $3–4 trillion by 2030, growing at roughly 40% a year, and even that aggressive forecast keeps looking conservative as demand for compute continues to outstrip supply across the board.

This is a look at the ten US companies actually building that infrastructure in 2026 — not the AI applications sitting on top of it, but the chips, cloud platforms, and physical buildout that make everything else possible.

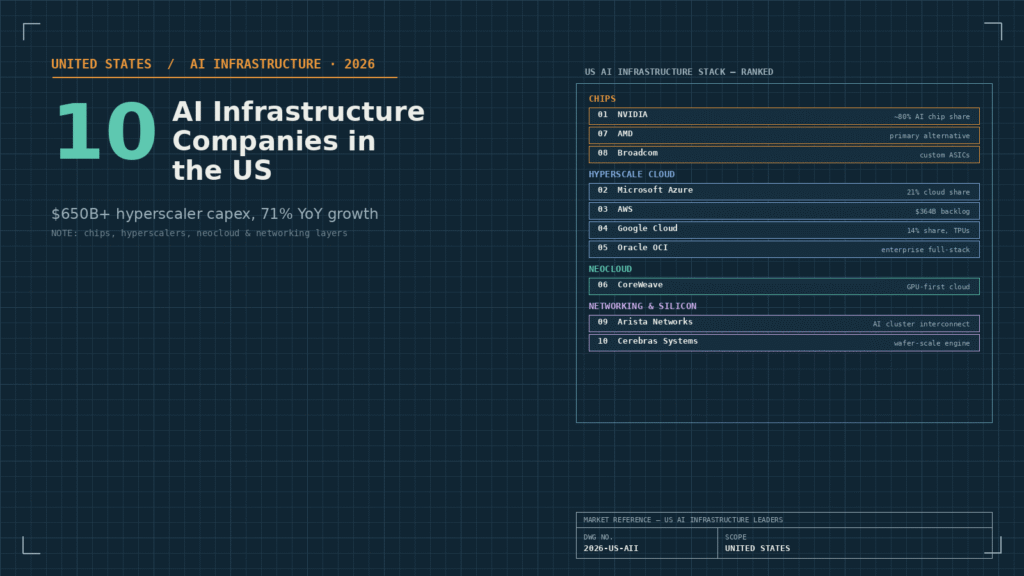

1. NVIDIA — The Chip Layer’s Center of Gravity

Nvidia controls roughly 80% of the global AI chip market as of 2026, and that dominance isn’t just about raw GPU performance — it’s the CUDA software ecosystem that keeps developers, frameworks, and enterprise infrastructure locked into Nvidia hardware by default. Q1 FY2027 results showed $81.6 billion in quarterly revenue with adjusted EPS of $1.87, beating consensus, and the company now carries a market cap near $5.4 trillion. The next catalyst is the Vera Rubin platform, landing in the second half of 2026, which management expects to stay supply-constrained for its entire lifecycle — demand simply isn’t slowing down enough to let inventory catch up.

2. Microsoft — Azure as the “AI-First” Cloud

Microsoft Azure holds a dominant 21% of the global cloud market, and 2026 has been defined by embedding Copilot into every layer of the stack to make Azure the most frictionless platform for enterprises operationalizing generative AI. To handle the power demands that come with that, Microsoft’s 2026 capital spending has gone specifically toward next-generation nuclear-powered data centers and advanced liquid cooling — infrastructure decisions that go well beyond just buying more chips.

3. Amazon — AWS’s Silicon-First Scale Play

AWS remains the world’s largest cloud infrastructure provider, and its 2026 roadmap centers on a “Silicon First” strategy: heavy investment in its own Trainium3 and Inferentia3 chips to give enterprise customers a more cost-effective path for LLM training and inference than GPU-only alternatives. The company’s committed backlog has reportedly reached $364 billion, with demand actively exceeding available capacity — a strong market position, but also a real procurement bottleneck for new customers trying to get in the door.

4. Alphabet — Google Cloud’s TPU Advantage

Google Cloud is the fastest-growing of the “Big Three” hyperscalers, now holding roughly 14% of the global cloud market. Its edge is vertical integration: proprietary Tensor Processing Units (TPUs) built specifically for AI workloads, paired with Alphabet’s data-intelligence expertise, give Google Cloud a differentiated position against AWS and Azure rather than just competing on the same GPU-rental terms.

5. Oracle — Enterprise AI Infrastructure From Austin

Oracle Cloud Infrastructure (OCI) has positioned itself as the enterprise-grade AI infrastructure option for organizations that want the full stack — data, analytics, security, and machine learning — under a single vendor rather than assembled from multiple providers. It’s a smaller footprint than the Big Three, but a deliberately differentiated one, targeting the enterprises whose compliance and integration requirements make a single-vendor approach worth the tradeoff.

6. CoreWeave — The Neocloud Leader

CoreWeave is the clearest example of the “neocloud” category: a cloud provider built specifically around GPU compute rather than general-purpose infrastructure with AI bolted on. Alongside Oracle Cloud Infrastructure and Lambda Labs, CoreWeave has become one of the go-to options for AI labs and enterprises that need large GPU clusters without competing for capacity against the hyperscalers’ own internal workloads.

7. AMD — The Primary Alternative to NVIDIA

AMD remains the most credible chip-level alternative to Nvidia’s near-monopoly, competing directly in the GPU and accelerator market as hyperscalers and enterprises look to diversify their compute supply chains and reduce single-vendor risk. It’s not close to displacing Nvidia’s CUDA ecosystem yet, but it’s the clearest pressure valve in the market for buyers negotiating pricing or managing supply-chain concentration risk.

8. Broadcom — The Custom Silicon Power Behind the Scenes

Broadcom has become one of the most important names in AI infrastructure without being a household one — building the custom ASICs and networking silicon that hyperscalers increasingly rely on to reduce dependence on off-the-shelf GPUs for specific inference workloads. As hyperscaler custom-silicon programs mature, Broadcom’s role as the enabling partner behind that shift keeps growing, even though it rarely appears in the same headlines as Nvidia or AMD.

9. Arista Networks — The Networking Layer That Makes Clusters Work

AI training runs at the scale hyperscalers now operate at only if thousands of GPUs can talk to each other fast enough — and that’s Arista Networks’ entire business. Arista leads AI data center networking in the US, providing the high-speed interconnects that turn a warehouse of individual chips into a single coordinated training cluster. It’s an easy layer to overlook, but a training run is only as fast as its slowest network hop.

10. Cerebras Systems — Betting Against the GPU Cluster Model

Cerebras takes the most architecturally different approach on this list: instead of clustering thousands of smaller GPUs, it builds AI supercomputing platforms around the Wafer-Scale Engine — reportedly the largest chip ever manufactured — specifically to sidestep the memory-bandwidth bottleneck that limits conventional GPU clusters. The company was valued at roughly $23 billion after a $1 billion Series H round in February 2026, led by Tiger Global, and counts OpenAI, Mistral AI, the Mayo Clinic, and DARPA among its customers. After withdrawing its IPO registration in late 2025 to refile with stronger financials, Cerebras is reportedly still planning to go public in 2026.

What the List Tells You About Where the Money’s Actually Going

Line these ten up and a pattern falls out that’s worth paying attention to beyond any individual company: US AI infrastructure spending is stacking across four distinct layers, not concentrating in one. Chip design (Nvidia, AMD, Broadcom, Cerebras) captures headlines, but hyperscale cloud (Microsoft, Amazon, Google, Oracle) is where the actual capital expenditure lands — hundreds of billions of dollars annually, increasingly directed at power and cooling infrastructure as much as compute itself. Neoclouds (CoreWeave) exist specifically because that hyperscaler capacity still can’t keep up with demand, and networking (Arista) is the layer that determines whether all that compute can actually work together at scale.

That layered structure is also the practical takeaway for any US enterprise evaluating where to build. The “right” infrastructure choice increasingly depends on workload type more than brand loyalty: hyperscalers for teams wanting the full data-and-security stack in one place, neoclouds for teams that need raw GPU capacity without hyperscaler queue times, and custom-silicon partners for organizations with inference workloads specific enough to justify moving off general-purpose GPUs entirely. Most mature US enterprises in 2026 aren’t picking one — they’re running a deliberate mix across two or three of these layers, matched to the workload rather than a single vendor relationship.

The Bottom Line for US Buyers

The capacity-constrained reality running through nearly every company on this list — Nvidia’s Vera Rubin platform, AWS’s $364 billion backlog, Microsoft’s nuclear-powered data center bet — points to the same underlying conclusion: demand for AI compute in the US is still outrunning supply in 2026, and it’s not close. For enterprises planning infrastructure spend this year, that means procurement timelines and capacity commitments deserve as much strategic attention as model selection or architecture decisions. The companies on this list are the ones building the floor everything else in American AI stands on — and right now, that floor is still being poured as fast as it can be.