Everyone is asking the same question in boardrooms, on trading floors, and in startup pitch meetings right now: Is AI a bubble — and if so, when does it pop?

The honest answer is uncomfortable. Yes, there are clear bubble-like characteristics in the AI investment landscape. But the timing of any correction is genuinely uncertain — and how bad it gets depends on factors still playing out in real time. What’s not uncertain is this: business leaders who understand what’s driving the tension are far better positioned than those who don’t.

Here’s a clear-eyed look at where things stand.

The Numbers That Should Make You Nervous

Let’s start with the math, because the math is stark.

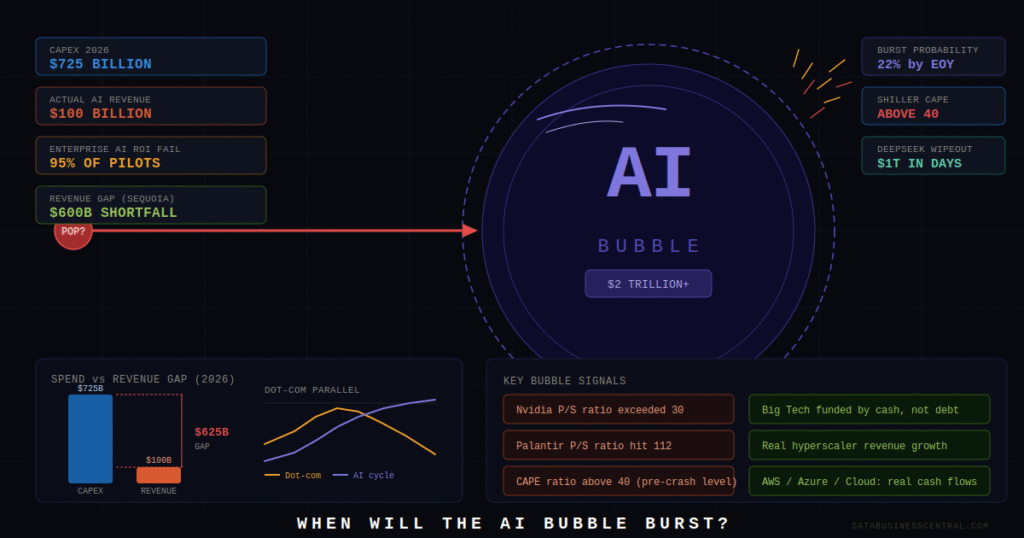

The five largest US technology companies — Microsoft, Amazon, Alphabet, Meta, and Oracle — have collectively guided toward $635–690 billion in AI capital expenditure for 2026, a 67–74% increase over 2025. Total Big Tech AI spending is projected to hit roughly $725 billion this year, with Goldman Sachs and Morgan Stanley projecting over $1 trillion by 2027. This is, in absolute terms, the largest private technology investment cycle in recorded history.

On the revenue side, the picture is far more modest. US consumer AI revenue stands at roughly $12 billion annually. Enterprise AI generates around $100 billion in actual revenue. An MIT study found that 95% of generative AI pilot programs fail to produce measurable business value, and only 5% of enterprises report significant earnings impact from AI investments — despite 78% of organizations now using AI in some capacity.

Sequoia Capital’s David Cahn calculated a $600 billion annual revenue gap between what the industry is spending and what it’s actually earning. That gap is widening, not closing, in 2026.

To put it in starker terms: one analysis comparing OpenAI’s infrastructure costs against its projected revenue found a $47 billion annual shortfall — $60 billion spent against $13 billion earned. When spend is running at more than four times revenue, that’s not an investment cycle. That’s a definition of a bubble.

How This Compares to the Dot-Com Era

The dot-com comparison gets made constantly, and for good reason — the patterns rhyme uncomfortably closely.

In the late 1990s, investors added “.com” to any business name and watched valuations soar. Today, adding “AI-powered” to a product description is often sufficient to raise tens of millions from venture capital. One recent case: an OpenAI executive launched a new company valued at $10 billion — no product, no customers, just a pitch deck.

Valuation multiples tell a similar story. Nvidia’s price-to-sales ratio has exceeded 30 at multiple points in recent months — a level that has historically proved unsustainable for even the fastest-growing technology companies. Palantir’s P/S ratio hit 112 in late 2025. The Shiller CAPE ratio for the broader market exceeded 40 in late 2025, a level previously seen only in the months before the dot-com crash.

When Morgan Stanley compared current hyperscaler AI capital expenditure to the dot-com era telecom boom — noting that it is set to exceed that boom in both magnitude and duration — that was not casual commentary. These are the kinds of comparisons serious analysts reserve for late-cycle warnings.

Prediction markets have taken notice. On Polymarket, the leading outcome for “AI bubble burst by…?” is priced at approximately 22% probability for end of 2026, with $2.9 million in trading volume backing those positions.

Why This Cycle Is Different from 2000 — In Both Good and Bad Ways

The dot-com analogy has important limits, and intellectually honest analysis requires acknowledging them.

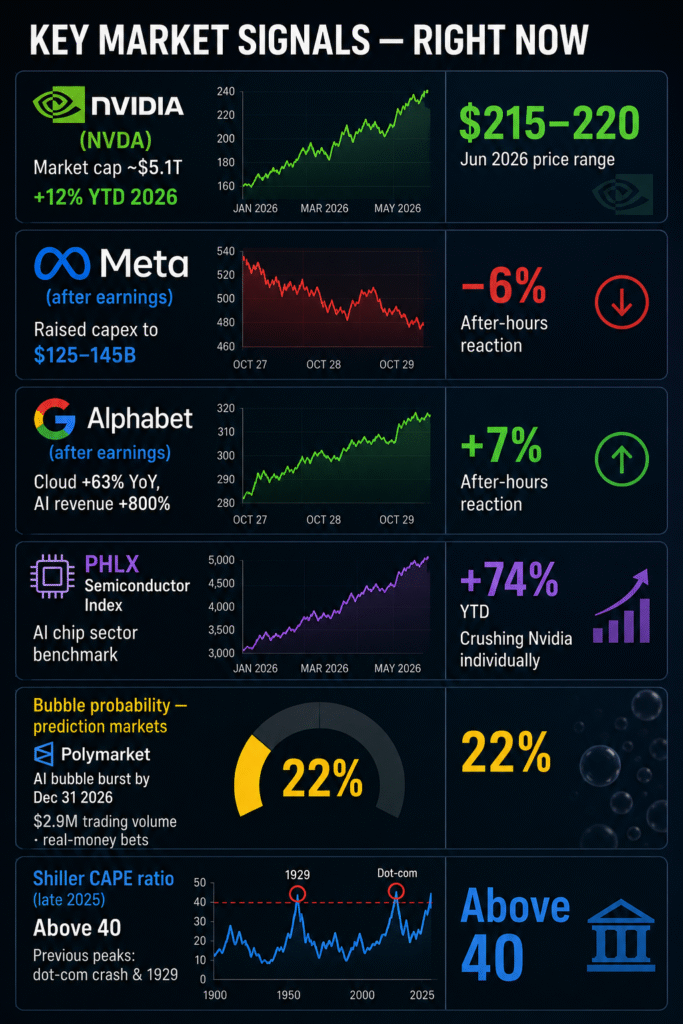

In 2000, most of the companies fueling the boom were pre-revenue, pre-profit, and in many cases pre-product. Today’s AI leaders are generating real and rapidly growing revenue. Nvidia reported $57 billion in revenue for fiscal Q3 2025, up 62% year-over-year, with $23.8 billion in operating cash flow in a single quarter. AWS is running at roughly $150 billion annualized. Google Cloud at $80 billion. Azure AI at $37 billion run-rate and growing at 123% year-over-year.

These are not dot-com era “eyeballs.” They are real cash flows. Fidelity’s research team, writing in early 2026, noted they are not seeing the classic late-bubble warning signs: free cash flows are not shrinking, leverage ratios are not deteriorating, and there is no broad debt-fueled expansion across the sector. Big Tech is funding most of its AI capex from existing operations, not borrowed money — a crucial difference from the telecom boom that preceded the dot-com crash.

The bear case, however, is that this structural advantage is concentrated in the very top of the pyramid. Below the hyperscalers, the picture changes rapidly. Thousands of AI startups and mid-market enterprises are burning cash against speculative revenue models, backed by venture capital that has grown increasingly impatient with the absence of returns.

The Trigger Events to Watch

Bubbles don’t burst on a schedule — they burst when a trigger breaks the narrative. Here are the most likely candidates for 2026 and into 2027:

Earnings disappointments. Q2–Q4 2026 earnings seasons will be the acid test. If hyperscalers report massive capital expenditure without corresponding revenue acceleration, Wall Street’s patience will snap. When Alphabet announced $175–185 billion in 2026 capex — roughly double 2025 levels — it triggered an immediate sell-off. Investors are already watching this ratio closely.

A second DeepSeek-type shock. In January 2025, the release of DeepSeek wiped nearly $1 trillion in market value in a matter of days, including a single-day 17% drop in Nvidia, erasing over $600 billion. The shock demonstrated that AI capabilities can be delivered at a fraction of assumed cost, instantly undermining the narrative that justifies massive infrastructure investment. A similar development — from a Chinese competitor, an open-source breakthrough, or a new efficiency model — could replay the same dynamics.

Startup failures at scale. The venture-backed AI startup layer is under serious pressure. CFOs are demanding ROI. The 18-month grace period that most AI startups received from investors is expiring. A wave of high-profile failures or down-rounds could shift sentiment quickly.

Regulatory pressure. The EU AI Act’s high-risk system compliance deadline is August 2026. Enforcement actions against major AI deployments could introduce costs and delays that compress the revenue timelines investors are counting on.

The Case That There Is No Pop — Just a Long Plateau

Not everyone sees a dramatic correction coming, and their arguments deserve a fair hearing.

Fidelity’s research team argues that the AI cycle more closely resembles the railroad or electrification buildouts than the dot-com boom — infrastructure investments that took decades to fully monetize but ultimately delivered transformative returns. The fact that today’s AI leaders have real cash flows, strong balance sheets, and funded capex cycles means the structural conditions for a catastrophic collapse are not clearly present.

Morgan Stanley’s analysts have suggested a 1–2% margin uplift from AI across the S&P 500 could ultimately justify the investment base, and that the more likely outcome is a sector rotation — investors moving from AI builders toward AI adopters as proof points emerge — rather than a broad market crash.

The most nuanced framing may be this: the capex side of the AI cycle has bubble-like characteristics. The revenue side is growing fast enough that calling the exact moment the gap closes — or snaps — is genuinely difficult. We may be in an overinvestment cycle that eventually resolves through productivity gains we cannot yet fully measure, rather than through a dramatic correction.

What This Means for Your Business

Whether the AI bubble deflates gradually or pops dramatically, the practical implications for business leaders are the same.

Stop measuring AI investment in inputs, not outputs. The enterprises that survive whatever comes next are those demanding measurable P&L impact from AI projects — not just adoption metrics, demos, and pilot programs. The 95% failure rate in enterprise AI pilots is not random. It reflects the absence of clear use-case definition, integration investment, and accountability structures.

Separate infrastructure from application. The risk of an AI correction is concentrated differently at different layers. Chip manufacturers and data center operators face the most exposure if spending slows. Enterprise software companies with proven AI-augmented products face far less. Know which layer your suppliers and partners sit in.

Be skeptical of valuations in your supply chain. If a vendor’s valuation is built on AI hype rather than demonstrated revenue, you carry counterparty risk. In a correction, overfunded AI startups do not quietly survive — they cut staff, abandon roadmaps, and sometimes disappear. Build this into your vendor risk assessments.

Don’t confuse the bubble with the technology. Even if the dot-com comparison holds, remember what the dot-com era actually produced: the infrastructure and companies that built the modern internet economy. Amazon, Google, and many of the most important businesses of the 21st century were either born in that correction or survived it. The AI bubble bursting — if it does — will not make AI less real. It will clear away the noise and reveal which use cases, and which companies, actually have durable value.

Real time data explaination

AI Bubble — Real-Time Data Dashboard

Sources: SEC filings, Q1 2026 earnings calls, Polymarket · Updated June 2026

Live earnings — Q1 2026 results (reported Apr–May 2026)

Nvidia Revenue -$81.6B , +85% YoY · Q1 FY2027

Nvidia Data Center-$75.2B ,+92% YoY · Blackwell ramp

Microsoft AI Revenue -$37B+ ,+123% YoY annualised run rate

Google Cloud -$20B ,+63% YoY · Q1 2026

2026 Big Tech AI CapEx — confirmed guidance

Amazon-$200B

Microsoft-$190B

Alphabet-$185B

Meta-$145B

TOTAL 2026 ~$725B

Up 77% from $410B in 2025 — largest private tech infrastructure cycle in history (Financial Times)

Bull vs bear — what the data says

BULL CASE — why it may not pop

Nvidia FY2026 full-year revenue: $215.9B (+65%). Microsoft Azure AI: +123% YoY. Google Cloud: +63%. Meta/Google ad revenue accelerating because of AI (+33% and +19% YoY). Big Tech funding capex from cash, not debt. Jensen Huang: “the buildout of AI factories — the largest infrastructure expansion in human history — is accelerating.”

BEAR CASE — why it might

$725B CapEx vs ~$100B AI end-user revenue = $625B annual gap. DRAM prices up 95% QoQ — driving cost inflation, not revenue. 95% of enterprise AI pilots produce zero measurable ROI. Meta fell 6% just for raising its capex — investor patience is conditional. Palantir P/S hit 112. CAPE above 40. One DeepSeek-level shock could reprice everything.

MOST LIKELY SCENARIO — plateau, not pop

Morgan Stanley and Fidelity both argue the real risk is sector rotation, not a crash. AI builders (chip/infrastructure) face compression. AI adopters showing measurable ROI will outperform. The $600B gap is a timing problem, not necessarily a fraud. But 2026 Q2–Q4 earnings will be the acid test. If revenue doesn’t start closing the gap, patience ends.

The Bottom Line

The AI investment landscape in 2026 presents a genuine paradox: the most consequential technology transition in a generation, being funded at a pace and valuation premium that history suggests is unsustainable.

The technology is real. The revenue gap is also real. The question is not whether a correction of some kind is coming — virtually every serious analyst acknowledges the tension — but whether it arrives as a sharp pop, a slow deflation, or a gradual rotation that rewards investors patient enough to hold through the noise.

For business leaders, the most dangerous position is the one at either extreme: dismissing AI as pure hype and missing the productivity gains it is already delivering in the right applications, or pouring capital into AI initiatives with no accountability for returns, assuming the investment cycle justifies any spending.

The companies that navigate what comes next will be the ones that never confused a bubble with a revolution.

DataBusinessCentral.com covers data strategy, AI investment, and business technology leadership. For more insights, explore our latest analysis.